Blog

Luxury Manhattan Market Report: March 2026

Kelly Robinson

Kelly Robinson

If February was a cocktail party, March was the debrief the next morning..

According to the latest Olshan Luxury Market Report, Manhattan signed 33 contracts at $4 million and above in the week of March 23-29, up from 29 the week before, and the first quarter was still tracking as the fourth-best opening in the last decade despite war headlines, rising mortgage rates, and stock-market nerves. In other words, luxury buyers did not leave the chat. They just got more selective.

The whole picture

By our count from the four March weekly reports, Manhattan signed 131 luxury contracts this month, down from 147 in March 2025, a roughly 10.9% year-over-year dip. That sounds softer, and it is, but not dramatically so. The month started with a blowout 43-contract week, then cooled to 26, before finding its footing again at 29 and 33 in the final two weeks. Multiple industry reports show February had actually been the bigger flex, with 123 luxury contracts and about $1.382 billion in asking-price volume, versus 114 contracts and about $955 million in February 2025. March, by contrast, looked more like a market catching its breath than one falling apart.

March’s implied average asking price per signed contract came in around $8.53 million, based on roughly $1.117 billion in total asking-price volume across those 131 contracts. That is down about 24.1% from February’s roughly $11.24 million average asking price per signed contract, which tells you exactly what happened: February was stuffed with trophy product and outsized sponsor deals, while March returned to earth. The good news is that March was still slightly above March 2025’s average monthly asking price of $8.33 million, so pricing did not collapse. It normalized. Multiple industry reports show February’s spike was driven by several “whopper” deals, especially new development inventory on the Upper East Side, which inflated the monthly average in a way March simply did not.

Days on market tell the emotional story of March better than almost anything else. The month opened fast, with one weekly average at 137 days, then climbed to 358, then 541, then 608 by the final week of the month. On a weighted basis, March averaged about 389 days on market. That is meaningfully slower than the start of the month, but still far better than the 823-day monthly average reported for March 2025. Translation: buyers are taking longer than they did a few weeks ago, but nowhere near as long as they were taking last March. The market is cautious, not catatonic.

Still condos. By a mile.

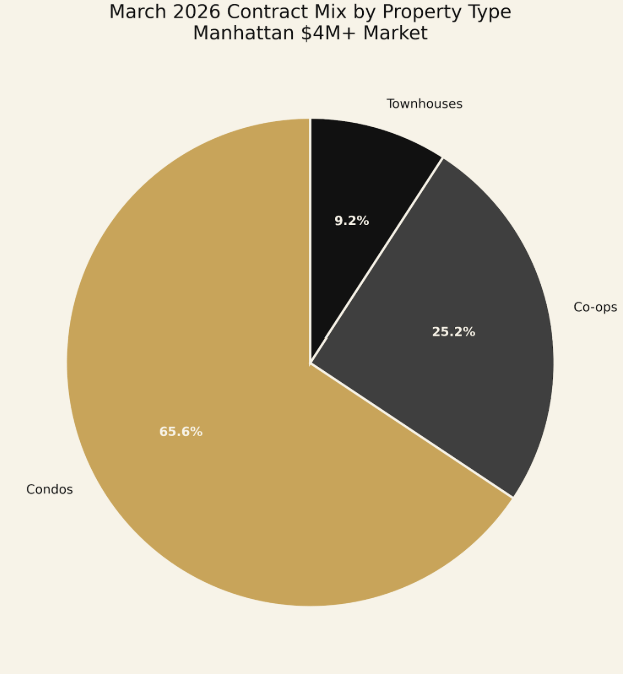

By our count, condos accounted for 86 of March’s 131 luxury contracts, or about 65.6% of the month’s activity. Co-ops came in second with 33 deals or roughly 25.2%, and townhouses trailed with 12 deals, just over 9%. Last March, condos were even more dominant, taking 112 of 147 contracts, or about 76.2%. So the pecking order has not changed, but the mix has softened a little: condos still lead, just not quite as aggressively as they did a year ago.

Why? Multiple industry reports show three big reasons. First, new development and sponsor inventory still disproportionately fuels condo activity, and March’s biggest deals were once again heavily condo- and sponsor-led. Second, condos are simply easier and more flexible to buy, especially for LLC buyers, pieds-à-terre purchasers, investors, and international capital. Third, co-ops still appeal to value-minded buyers who want pedigree and square footage, but their stricter board process and lower flexibility naturally narrow the buyer pool. Townhouses remain the boutique category: glamorous, scarce, and loud when they trade, but never the volume engine.

The March luxury market was not weak. It was disciplined. February had trophy heat, sponsor momentum, and headline-friendly volume. March had a little less swagger and a little more scrutiny. Asking prices came off February’s sugar high, days on market stretched out as the month progressed, and condos remained the undisputed volume leader, even if co-ops held a bit more share than they did a year ago. Multiple industry reports show the same broader message: Manhattan luxury is still trading, still resilient, and still attracting serious money, but buyers are rewarding the right product, not every product.

March did not kill momentum. It filtered it.

The buyers are still there. The deals are still getting done. But the market has stopped applauding itself quite so loudly. Condos remain the star, co-ops are quietly taking a few more lines, and townhouses are still the dramatic cameo. Manhattan luxury is not in retreat. It is just acting like grown-ups are finally back in the room.

Check out our latest real estate listings from the team in more areas in New York City

Known for their attention to detail and collaborative work style, the One Global Advisory Team works to ensure their clients are expertly represented every step of the way.

CONTACT US